Starting 1 January 2025, significant changes came into effect concerning VAT deduction adjustments for overdue receivables on the side of the debtor, based on Section 74b of the Czech VAT Act (Act No. 235/2004 Coll., as amended). These changes introduce a new obligation for VAT-registered debtors to reduce their previously claimed input VAT if payment for a taxable supply has not been made within a specified period.

Scope and Purpose of the Amendment

This new obligation applies only to input VAT deductions arising from taxable supplies received on or after 1 January 2025. It is important to distinguish this from the creditor’s right to adjust VAT on irrecoverable receivables under Sections 46 et seq. of the VAT Act, which remains unchanged.

The legislative change was introduced to align with EU case law (e.g. CJEU Case C-335/19 E.), allowing member states to require VAT deduction adjustments even before insolvency or liquidation proceedings begin, in order to mitigate the risk of revenue loss for the state.

When Is the VAT Deduction Adjustment Required?

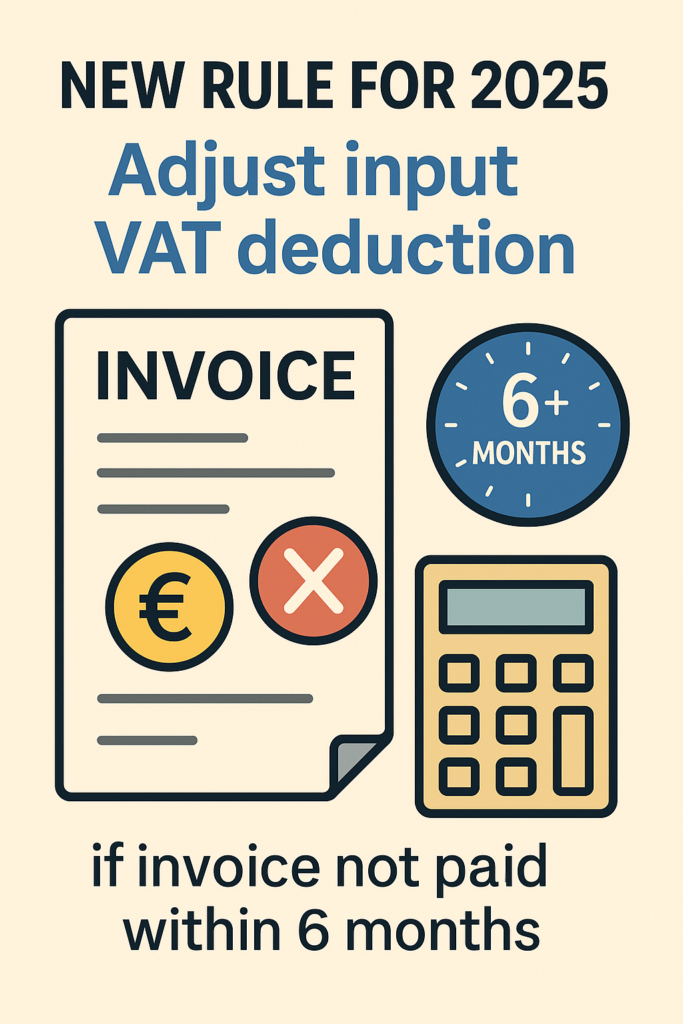

Under the new Section 74b(3) of the VAT Act, a VAT-registered debtor must reduce the previously claimed VAT deduction if:

The invoice remains unpaid, and

Six full calendar months have passed since the due date of the invoice (as agreed in the contract, general terms, or by law).

The adjustment must be made in the VAT return for the tax period in which the 6-month period ends. The reduction is calculated based on the unpaid portion of the taxable amount.

Right to Increase the VAT Deduction Upon Payment

If the debtor later settles the invoice in part or in full, Section 74b(4) allows them to increase their input VAT deduction again. This must be reported in the tax period in which the payment was made (based on the date funds were debited from the debtor’s account) and no later than the end of the second calendar year following the adjustment.

Special Rule for Quarterly Taxpayers

For taxpayers filing quarterly VAT returns, the obligation to reduce the VAT deduction does not arise if the debt is fully paid by the end of the same quarter in which the 6-month overdue threshold is met. This is to prevent situations where a deduction must be decreased and immediately increased within the same period.

Practical Considerations and Common Scenarios

The GFŘ issued a guidance on this topic and it clarifies the following:

The new rules apply only to supplies where the supplier is liable for VAT (i.e. not to reverse charge supplies).

If only part of a receivable is overdue, the deduction must be reduced only proportionally.

Offsets (mutual debt settlements) are treated as payments.

If the receivable is assigned to another party and later paid, the debtor may still increase their VAT deduction.

The adjustment must reflect the applicable VAT rates or proportional use (e.g. under §§ 75–76).

Ongoing complaint or warranty procedures do not exempt the debtor from the adjustment unless they result in an official price reduction (credit note).

Example

A debtor receives a taxable supply on 15 March 2025, due 15 April 2025, and pays it fully on 15 November 2025.

If the taxpayer files monthly VAT returns, the deduction must be reduced in October 2025 and may be increased again in November 2025.

If filing quarterly, and the payment occurs in Q4 2025, no reduction is needed.

Conclusion

These changes impose a new compliance obligation on VAT-registered debtors in the Czech Republic. Businesses should update their accounting processes to monitor overdue invoices and ensure timely adjustments to VAT deductions. Accurate records of due dates and payment settlements will be essential to fulfil these obligations and avoid penalties.

If you need help understanding how these new rules apply to your business or require support with VAT compliance, feel free to contact us at Expat-Tax.cz.